Find out how an ABLE account can enhance financial security and provide essential support for those with disabilities.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/Bp7mLDSeHM0

Focusing on the advantages and disadvantages of life insurance settlements is an important topic to discuss today. We see the many tv commercials espousing the benefits of selling your life insurance policy, but there are advantages and disadvantages to selling and there may be other options to consider, as well.

Life Settlement

A life settlement is the sale of a life insurance policy to a third party. The owner of a life insurance policy sells it for a cash payment that is less than the full amount of the death benefit. The buyer becomes the new owner and/or beneficiary of the life insurance policy, pays all future premiums and collects the full amount of the death benefit when the insured dies.

This is different than a viatical settlement which is when an individual with a terminal or chronic illness sells his or her life insurance policy. There are different tax consequences depending upon the type of settlement.

Can anyone sell their insurance policy?

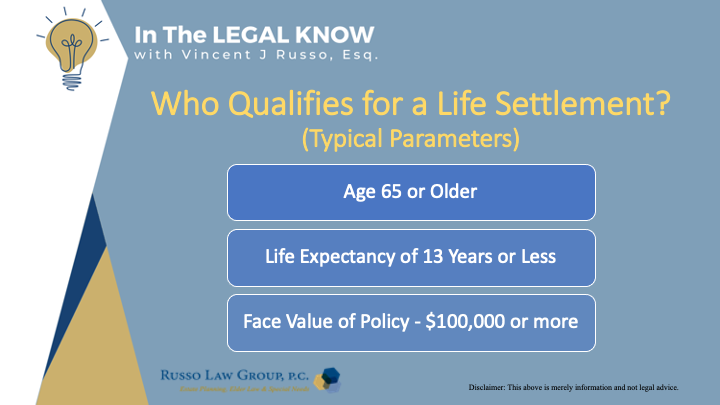

The following are the typical parameters required for a life settlement.

The policy must be at least two years old, and the death benefit must be at least $100,000 or more. In most cases, the minimum age to qualify for a life settlement is 65 years old. Typically, the older you are, the more likely you are to qualify for a life settlement.

However, age is not the only factor that determines your eligibility. The most suitable candidate for a life settlement is one with a life expectancy of less than 13 years.

Typically, policy premiums need to be less than 5% of the policy’s face amount. The policy must be either a universal life, convertible term, variable life, whole life, or second to die policy to qualify for a life settlement. Just about any life insurance policy can be sold.

Reasons to consider when selling a life insurance policy.

There are several reasons why someone might want to sell the policy.

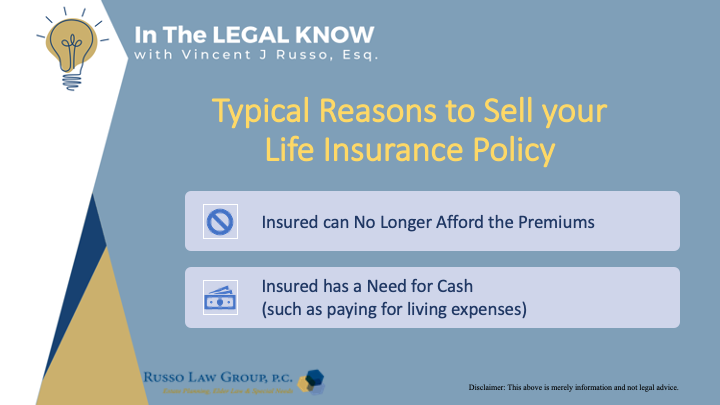

Two typical reasons are:

- The insured can no longer afford the premiums.

- The insured has a need for cash (such as paying for living expenses).

In the way of background, it is estimated that as many as 90% of life insurance policies are allowed to lapse by the holders before the time of their death.

Pros and cons of selling a life insurance policy.

Like anything in life, there are advantages and disadvantages to selling a life insurance policy.

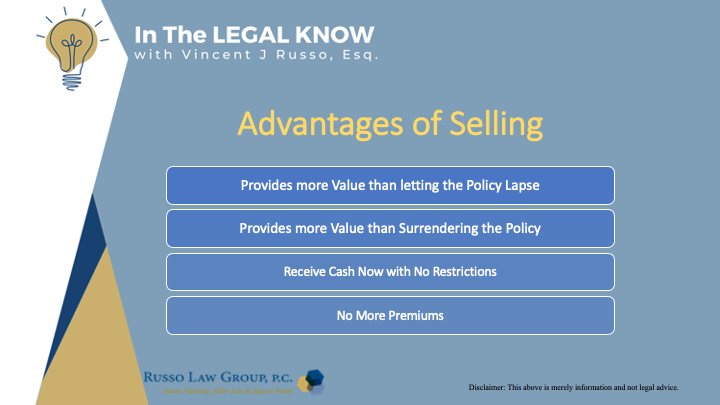

When it comes to life settlements, some of the pros include:

- Provides more value to you than letting your policy lapse or surrendering your policy.

- Receive one lump sum of cash to use however you want, no restrictions.

- No more premiums.

Now, let’s look at the disadvantages.

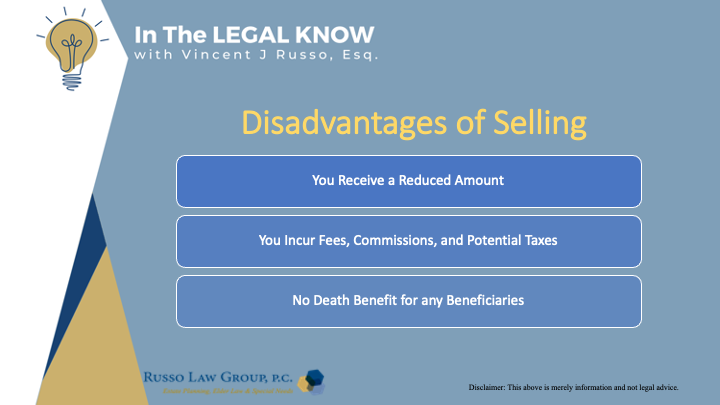

The cons of a life settlement can include things like:

- No longer owning your policy. The amount you receive will range from 10 to 30% of the value of the death benefit.

- Incurring taxes on your lump sum of cash.

- Potential fees and commissions during the sale of your policy.

- No death benefit for any beneficiaries

Key questions when considering what to do with a life insurance policy.

- Do I still need life insurance protection?

- Will I need and qualify for a new life insurance policy in the future?

- If I sell my policy, how will they decide how much will I actually receive after taxes and costs

Other Options

There are a number of options available to the owner of a life insurance policy:

- Find out if you have any cash value in your life insurance policy. You may be able to use some of the cash value to meet your immediate needs and keep your policy in force for your beneficiaries without having to sell it to a third party. You may also be able to use the cash value as security for a loan from a financial institution.

- Review other sources of cash that may meet your financial needs at a lower cost than a life settlement.

- Know that your creditors could claim the proceeds.

- Find out if you’ll lose any public assistance benefits such as food stamps or Medicaid if you get a cash settlement.

I would suggest contacting your insurance, agent, financial advisor, and a professional tax advisor to fully understand your options and the consequences of selling your insurance policy.

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Related Posts

Comments (0)