Find out how an ABLE account can enhance financial security and provide essential support for those with disabilities.

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/wwupVCDdMAY

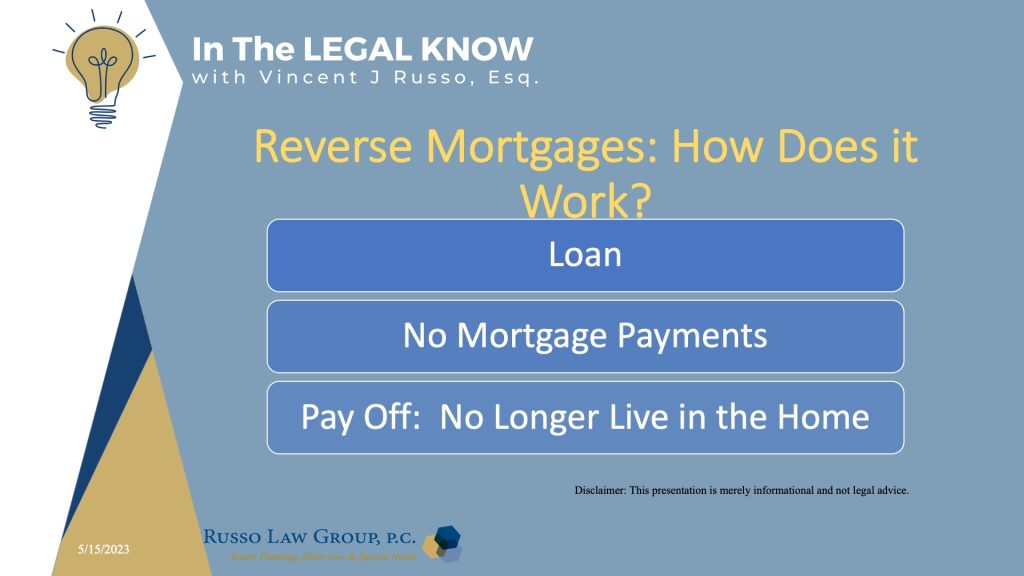

What is a Reverse Mortgage?

A reverse mortgage loan is like a traditional mortgage.

Homeowners borrow money from a lender using their home as security for the loan. Also like a traditional mortgage, when you take out a reverse mortgage loan, the title to your home remains in your name.

However, unlike a traditional mortgage, with a reverse mortgage loan, borrowers don’t make monthly mortgage payments. The loan is repaid when the borrower no longer lives in the home. Interest and fees are added to the loan balance each month and the balance owed grows.

How is it possible to get a mortgage with no payments.

Normally, when you take out a mortgage loan, the bank gives you a lump sum that you pay back with interest over time. At the end of the term, the loan is paid down to $0.

A reverse mortgage works in, well, reverse. The lender actually makes payments to you: you can choose to receive a lump sum, monthly payments, a line of credit or some combination of those options.

The interest and fees associated with the loan get rolled into the balance each month. That means the amount you owe grows over time, while your home equity decreases. You get to keep the title to your home the whole time, and the balance isn’t due until you move out or die.

When that time comes, proceeds from the home’s sale are used to pay off the debt. If there’s any equity left over, it goes to the estate. If not, or if the loan is actually worth more than the house, the heirs aren’t required to pay the difference. Heirs also can choose to pay off the reverse mortgage or refinance if they want to keep the property.

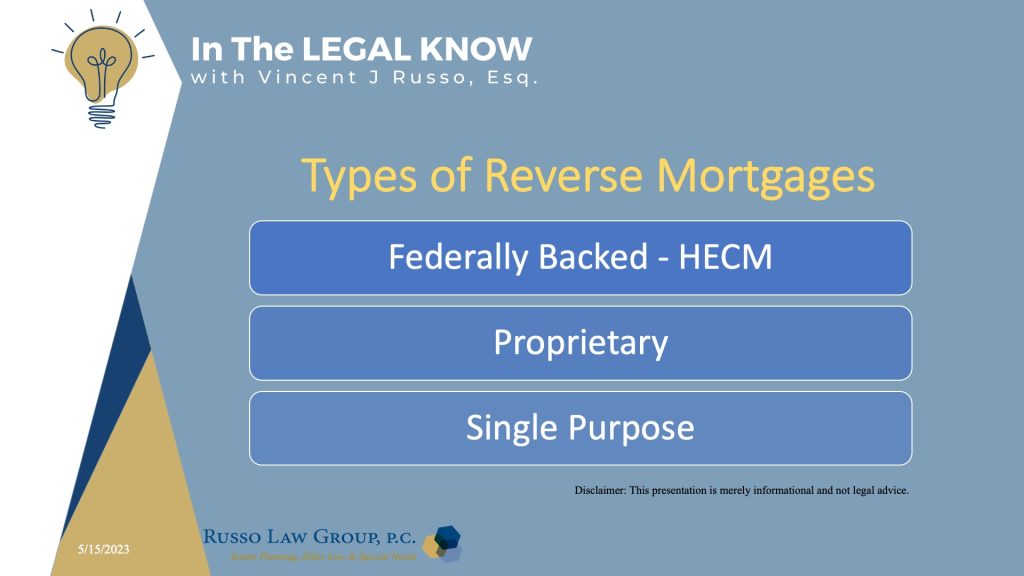

Are there different types of reverse mortgages?

There are basically Government backed loans, private loans, and single purpose loans.

The most common type of reverse mortgage is called a Home Equity Conversion Mortgage (HECM). These loans are backed by the Federal Housing Administration (FHA).

A proprietary reverse mortgage is a second option but these loans are not backed by the federal government so they are riskier. You also need to be careful as to the interest rates being charged.

Single Purpose Loans are loans to be used for a lender-approved purpose such as paying property taxes or performing maintenance on the home. So, there is a limitation on what you can use the funds for.

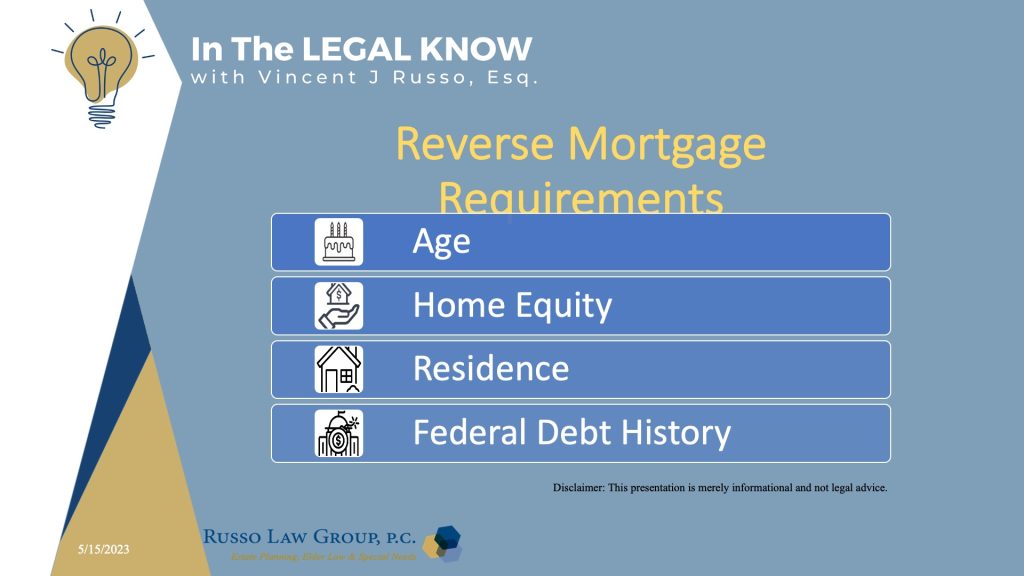

Can anyone qualify for this type of mortgage?

No, not everyone. There are several requirements:

- Age. You must be at least 62 years old. But although many people think of a reverse mortgage as a way for people to bridge the gap between age 62 and 66 (full retirement age), if you wait until age 66, you’ll be able to get a higher payout. If a private lender, the age can be as a low as age 55 (depending on state law).

- Home equity.You must own the home outright or have significant equity (at least 50%).

- Residence. The home must be your primary residence.

- Federal debt history. Delinquent federal debt, like income taxes or student loans, can make you ineligible for a reverse mortgage.

It appears that reverse mortgages are for seniors. Are there any other requirements?

This program is for seniors and there some other requirements.

- Housing counseling. You’re required to undergo counseling with a HUD-approved reverse mortgage counselor.

- Primary Residence. You must continue to use your home as your principal residence.

- Property upkeep.You must continue to keep the home in good condition.

- Taxes and insurance.It’s crucial to stay on top of your ongoing property taxes and homeowner’s insurance — otherwise you could lose your house to a property-tax lien foreclosure.

You can have co-borrowers (for example a married couple) but both of them would need to meet the requirements. The pay out would be based on the youngest borrower’s age.

You can also have one spouse be the sole borrower and the loan will not have to be satisfied until both spouses pass if the spouse meets certain requirements.

Click here to download our free informational pamphlet on Reverse Mortgages

Want to learn more about reverse mortgages?

Click here to read PART 2

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Related Posts

Hi there! Your website’s content on reverse mortgage is top-notch. Your blogs are a testament to your expertise in the field. I’m thrilled to have found your website and can’t wait to consume more of your insightful content. Keep up the brilliant work!

I resonate so deeply with the topic of this blog post. Here are my thouhts about your blog on Equity Line of Credit. Reverse mortgage loan provide a flexible financial tool for homeowners. They allow you to leverage your home’s equity for various needs, like home improvements or debt consolidation. Understanding the terms and responsible management are key to making the most of this valuable financial resource.