This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/aQgwbQkJtC0 How can SSI…

Selling Your Residence and the Capital Gains Exclusion

This originally aired on the Catholic Faith Network’s show CFN Live: https://youtu.be/aUe67RxG1gM

This is a very timely topic in light of us being in tax season. If you sold your home in 2022, you must report the sale on your personal income tax return and pay any taxes owed by April 18, 2023.

Will the sale of the home be taxed?

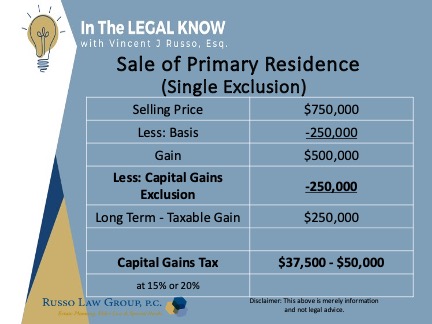

First, we need to do a calculation. There are several components to the calculation: Selling Price (the net selling price), Basis (cost of the home plus improvements), and the Tax Rate. And one more – the capital gains exclusion amount.

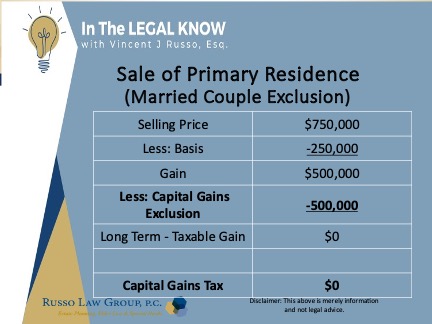

This is a wonderful tax break for a homeowner who sells their primary residence. If you own and use the residence as your primary residence 2 out of the last 5 years, then you qualify for a capital gains exclusion of $250,000 and if married, $500,000.

Let’s first look at an example of a single taxpayer who qualifies for the Capital Gains Exclusion.

Now, let’s look at an example of a married couple who qualify for the Capital Gains Exclusion.

If you do not qualify for the capital gains exclusion, taxes will be dramatically higher. In my example, the capital gains tax could be up to $100,000.

It is important to note that a taxpayer may not qualify because it was not their primary residence, or they did not own or use the residence two out of the last five years.

Planning to qualify should not be overlooked before you sell your primary residence.

What if you already took advantage of the exclusion on a former home, can you take it again on your primary residence?

Absolutely, if you meet the qualifying rules. You cannot qualify if you took advantage of the capital gains exclusion within two years of the current sale.

Also, there are exceptions to qualifying. For example, the rules are more liberal if you are a widower or divorced or entered a nursing home. One may also qualify for a partial exclusion: for example, if you had a work related move or health related move.

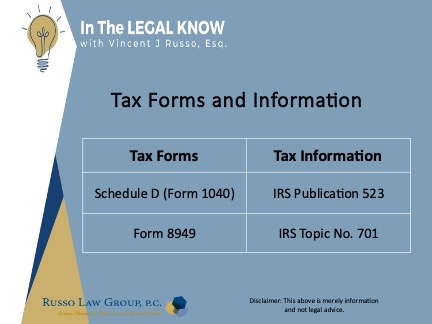

What form do you use to report the sale of your residence?

If you receive an informational income-reporting document such as Form 1099-S, Proceeds from Real Estate Transactions, you must report the sale of the home even if the gain from the sale is excludable.

Additionally, you must report the sale of the home if you can’t exclude all your capital gain from income.

Use Schedule D (Form 1040), Capital Gains and Losses and Form 8949, Sales and Other Dispositions of Capital Assets when required to report the home sale.

IRS Publication #523 and IRS Topic No. 701Sale of Your Home can be very helpful in understanding the rules. Since a lot of money can be involved here, you may want to contact a tax professional for assistance.

It is worthwhile to seek the services of a professional tax advisor if you sold your home and now need to report the sale on your tax return.

We hope you found this article helpful. Contact our office today at 1 (800) 680-1717 and schedule an appointment to discuss what makes sense for you and your loved ones.

Related Posts

This Post Has 0 Comments